Injury Settlement

In the aftermath of a personal injury, seeking compensation for your losses is crucial. Injury settlements offer a means to resolve disputes and obtain financial recovery without the need for lengthy and costly legal proceedings. These agreements involve negotiations between the injured party and the party responsible for their injuries, often facilitated by an attorney. Understanding the intricacies of injury settlements is essential for maximizing your recovery.

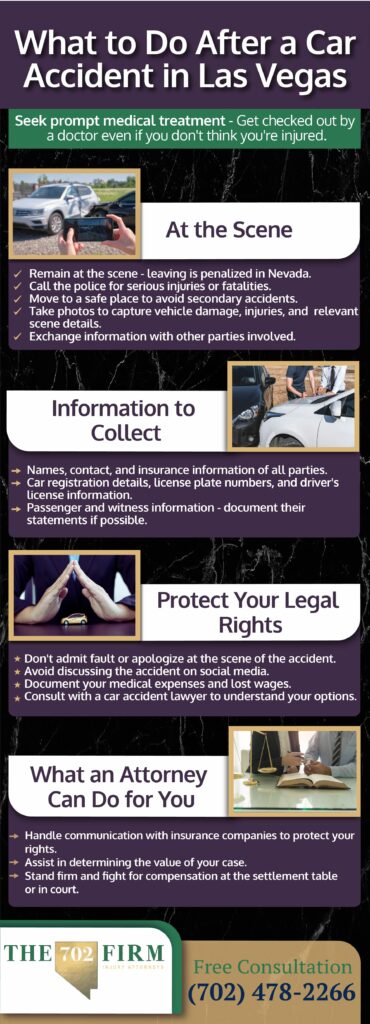

For instance, let’s consider a scenario where you suffer severe injuries in a car accident caused by a negligent driver. The driver’s insurance company may offer you an injury settlement to compensate for your medical expenses, lost wages, and pain and suffering. Accepting this settlement would require you to waive your right to pursue further legal action against the driver.

Factors Influencing Injury Settlement Amounts

The amount of an injury settlement varies depending on several key factors. These include the severity of your injuries, the extent of your medical expenses, the impact on your income and earning capacity, and the degree of pain and suffering you’ve endured. Additionally, the strength of your case, the insurance coverage available, and the skill of your attorney play significant roles in determining the settlement amount.

Calculating the appropriate settlement amount requires careful consideration of both economic and non-economic damages. Economic damages encompass medical bills, lost wages, and other out-of-pocket expenses directly related to your injuries. Non-economic damages, on the other hand, compensate for intangible losses such as pain and suffering, emotional distress, and loss of enjoyment of life.

Negotiating a fair injury settlement is a complex process that involves weighing the pros and cons of accepting a settlement offer versus pursuing a lawsuit. It’s advisable to seek guidance from an experienced attorney who can navigate the legal complexities and advocate for your best interests throughout the settlement process.

Injury Settlement: A Comprehensive Guide

If you have sustained injuries due to someone else’s negligence, navigating the legal process to obtain a fair injury settlement can be daunting. This guide will provide a comprehensive overview of the steps involved, empowering you to understand and advocate for your rights.

Introduction

Suffering an injury can be a traumatic experience, both physically and emotionally. Adding the complexities of the legal system can further compound the stress and uncertainty. However, understanding the process and partnering with an experienced attorney can equip you with the knowledge and support to navigate this challenging time.

Steps Involved in an Injury Settlement

Negotiation

The initial step in an injury settlement is negotiation. Your attorney will engage with the insurance company representing the at-fault party to discuss a fair settlement amount. Negotiations often involve back-and-forth offers and counteroffers based on the severity of the injury, medical expenses, lost wages, and other factors. To strengthen your negotiation position, it is crucial to document your injuries thoroughly, gather medical records, and keep accurate records of any expenses incurred.

Mediation

Mediation is a common step in the settlement process. A neutral third party, known as a mediator, facilitates a structured discussion between the parties. The mediator’s goal is to help both sides reach a mutually acceptable agreement. Mediation can be particularly beneficial when negotiations have reached an impasse, allowing for a fresh perspective and a focused environment.

Litigation

If negotiations and mediation fail to produce a fair settlement, your attorney may advise filing a lawsuit. Litigation is a significant step that involves formal court proceedings and can be lengthy and costly. However, it may be necessary to protect your rights and pursue the compensation you deserve. Your attorney will guide you through the legal process, representing your best interests in court.

Conclusion

Navigating an injury settlement can be a complex process, but with the right knowledge and support, you can empower yourself to seek justice and fair compensation. Remember to document your injuries and expenses, partner with an experienced attorney, and be prepared to negotiate and advocate for your rights throughout the process.

**Settlement in a nutshell: Know the injury, Know the money**

An injury settlement is a form of compensation awarded to individuals who have suffered physical or emotional harm due to the negligence or wrongful actions of another party. The amount of the settlement can vary significantly depending on various factors. As we delve into the details, let’s uncover what influences the size of your settlement check.

Factors Influencing Settlement Amount

The severity of the injury is one of the most significant factors affecting the settlement amount. Understandably, more severe injuries warrant higher compensation. The extent of medical treatment required, the impact on your daily life, and the potential for future complications are all taken into account. Think of it like a sliding scale: the more severe the injury, the higher the settlement.

Liability plays a crucial role in determining fault and, consequently, the settlement amount. If the other party is deemed solely responsible for your injuries, you’re likely to receive a larger settlement. However, if you share some degree of responsibility, the settlement amount may be reduced proportionately. It’s like a tug-of-war: the more liable the other party, the heavier your settlement.

Insurance coverage is another key factor. The amount of insurance coverage available to the at-fault party sets a ceiling for the potential settlement. If the insurance policy has a high coverage limit, you may be entitled to a larger settlement. On the other hand, if the coverage is limited, your settlement may be constrained. Picture a cup: the size of the insurance coverage determines how much settlement you can fill into it.

Legal fees can also impact the settlement amount. Attorneys typically charge a percentage of the settlement as their fee. This means that a higher settlement amount could result in higher legal fees. It’s like a trade-off: the bigger the settlement, the bigger the bite lawyers take.

Can I Get an Injury Settlement?

If you’ve been injured due to someone else’s negligence, you may be wondering if you can get an injury settlement. The answer is: it depends. There are a number of factors that will affect your chances of getting a settlement, including the severity of your injuries, the liability of the other party, and the insurance coverage available.

Benefits of Settling Early

If you’re eligible for an injury settlement, there are a number of benefits to settling early.

-

Financial relief. A settlement can provide you with much-needed financial relief, especially if you’ve lost income due to your injuries.

-

Reduced stress. The legal process can be stressful and time-consuming. Settling early can help you avoid the stress of a trial and get on with your life.

-

Avoid lengthy legal battles. Trials can take months or even years to complete. Settling early can help you avoid the uncertainty and expense of a lengthy legal battle.

Factors to Consider When Settling

If you’re considering settling your injury claim, there are a number of factors you should consider:

-

The severity of your injuries. The more serious your injuries, the more likely you are to get a fair settlement.

-

The liability of the other party. If the other party was clearly at fault for your injuries, you have a stronger case for a settlement.

-

The insurance coverage available. The amount of insurance coverage available will affect the size of your settlement.

-

Your own financial needs. You should also consider your own financial needs when deciding whether to settle. If you need money to pay for medical bills or lost income, you may be more likely to accept a lower settlement offer.

Tips for Negotiating a Settlement

If you’re negotiating a settlement, there are a few things you can do to increase your chances of getting a fair deal:

-

Be prepared. Gather all of your evidence and documentation before you start negotiating. This includes medical records, bills, and any other documents that support your claim.

-

Be realistic. Don’t expect to get everything you ask for. Be prepared to compromise and negotiate a settlement that is fair to both parties.

-

Don’t be afraid to walk away. If you’re not happy with the settlement offer, don’t be afraid to walk away. You may be able to get a better offer from another insurance company or by filing a lawsuit.